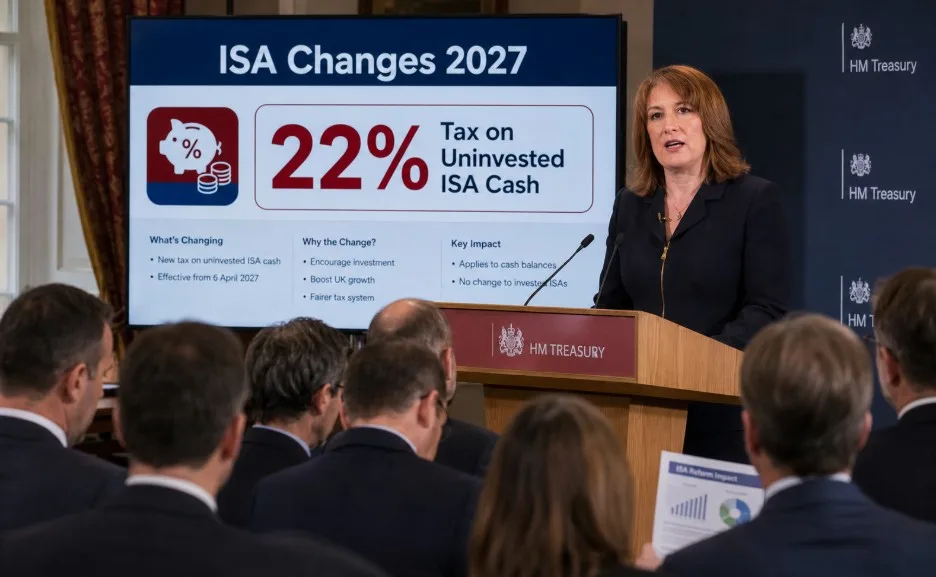

The proposed Rachel Reeves Investment ISA Levy is one of the most debated UK savings reforms in recent years. Under plans expected to take effect from April 2027, interest earned on uninvested cash held within a Stocks and Shares ISA could face a 22% tax charge.

The measure is designed to prevent savers from using investment ISAs as a workaround for reduced Cash ISA limits while encouraging greater participation in long-term investing.

Key highlights:

- A proposed 22% charge could apply to interest earned on uninvested ISA cash.

- The changes are linked to reforms to Cash ISA allowances for under-65s.

- The overall annual ISA allowance would remain £20,000.

- A reported “1p loophole” has sparked industry debate.

- Financial experts and investment platforms have raised concerns about complexity and implementation.

What Is the Rachel Reeves Investment ISA Levy and Why Is It Making Headlines?

The Rachel Reeves Investment ISA Levy refers to a proposed 22% tax charge on interest generated from uninvested cash held within Stocks and Shares ISAs. The policy has attracted significant attention because ISAs have traditionally been viewed as tax-efficient savings and investment vehicles.

The proposal follows concerns that savers may attempt to bypass future Cash ISA restrictions by placing excess savings into a Stocks and Shares ISA while leaving the money uninvested.

By taxing interest on cash balances, the Government aims to encourage investment activity rather than cash accumulation within investment accounts.

“The objective is to ensure investment ISAs are primarily used for investing rather than as alternative cash savings vehicles.” – Treasury Policy Statement

The proposal also revives comparisons with pre-2014 ISA rules, when cash interest within Stocks and Shares ISAs faced a similar levy before being abolished as part of broader ISA simplification reforms.

Why Does the Government Want to Tax Uninvested Cash Inside Stocks and Shares ISAs?

The Government argues that the reform supports its wider goal of creating a stronger investing culture while directing more capital into UK businesses and financial markets.

The Treasury’s Anti-Circumvention Strategy

The proposed levy is being presented as an anti-circumvention measure. Officials are concerned that savers could exploit a reduced Cash ISA allowance by moving excess cash into a Stocks and Shares ISA while continuing to earn tax-free interest.

Without additional restrictions, many investors might simply use investment ISAs as an alternative savings account rather than investing in shares, funds, or bonds.

How the Reduced Cash ISA Allowance Connects to the Levy?

The proposed 22% Investment ISA Levy does not exist in isolation; it forms part of a broader package of ISA reforms aimed at reshaping how UK savers allocate their annual tax-free allowance.

ISA allowance comparison:

| Feature | Current Rules | Proposed From April 2027 |

| Total ISA Allowance | £20,000 | £20,000 |

| Cash ISA Allowance (Under 65) | £20,000 | £12,000 |

| Cash ISA Allowance (Over 65) | £20,000 | £20,000 |

| Stocks and Shares ISA | Flexible | Subject to new cash-interest rules |

By maintaining the overall ISA limit while reducing the cash component, policymakers hope to encourage greater participation in investment markets. However, critics argue that this approach may disproportionately affect cautious savers.

How Will the New 22% Investment ISA Tax Work from April 2027?

Although final HMRC guidance is still awaited, the proposed framework suggests that interest earned on uninvested cash within Stocks and Shares ISAs would become subject to a 22% charge.

The proposal is expected to apply to cash balances sitting within investment platforms rather than funds actively invested in financial markets. Questions remain over how certain cash-like investments, including money market funds and short-duration instruments, will be classified.

Illustrative example of potential impact:

| Cash Balance | Interest Rate | Annual Interest | 22% Charge | Net Interest |

| £10,000 | 3.8% | £380 | £83.60 | £296.40 |

| £10,000 | 2.5% | £250 | £55.00 | £195.00 |

| £20,000 | 3.8% | £760 | £167.20 | £592.80 |

The practical impact will vary depending on interest rates, account structures, and future HMRC guidance. As a result, investors should avoid making major changes until final rules are confirmed.

Who Will Be Most Affected by the Rachel Reeves Investment ISA Levy?

The proposed ISA changes are expected to impact some savers and investors more than others, particularly those who rely heavily on cash holdings within ISA accounts. While not everyone will experience major changes, certain groups could face greater adjustments.

Groups Most Likely to Be Affected

- Under-65 savers: Those aiming to maximise cash savings within ISA allowances could see the biggest impact.

- Short-term investors: People using Stocks and Shares ISAs to temporarily hold cash may face restrictions.

- Cash-focused portfolio holders: Investors keeping large cash balances for flexibility could be affected.

- Strategic investors: Those waiting for market opportunities while holding cash reserves may need to rethink strategies.

- ISA providers and platforms: Firms may face extra monitoring and reporting responsibilities.

Older savers may see fewer changes, as current proposals suggest over-65s could keep existing Cash ISA allowances. Cash remains an important tool for many investors managing risk and market uncertainty.

Could the 1p Loophole Allow Savers to Avoid the 22% ISA Charge?

One of the most discussed parts of the proposed Rachel Reeves Investment ISA Levy is the reported “1p loophole,” which has gained attention among investors and financial experts. The issue focuses on stopping savers from using Stocks and Shares ISAs as alternatives to Cash ISAs if under-65 Cash ISA limits are reduced.

Under the proposals, interest earned on uninvested cash inside a Stocks and Shares ISA could face a 22% charge from April 2027. However, reports suggest investors could avoid this by holding a very small qualifying investment while keeping most funds in cash-like assets.

How the Reported Loophole Works?

The loophole depends on whether an account is fully cash-based or includes investments. Reports suggest savers could buy a tiny amount of shares and place most remaining funds into money market funds or similar assets.

Because the account would technically contain an investment, it may avoid rules targeting cash-heavy portfolios. This could allow investors to keep cash-like returns without triggering the proposed charge.

Potential example:

| Investment Structure | Amount |

| Actual Shareholding | £0.01 |

| Money Market Fund Holdings | £19,999.99 |

| Total ISA Value | £20,000 |

In practice, savers could use their reduced Cash ISA allowance first and place remaining funds into a Stocks and Shares ISA while keeping most holdings in low-risk products.

Why HMRC May Need to Tighten the Rules?

If widely used, the loophole could reduce the impact of the reforms. HMRC may need stricter definitions around qualifying investments and cash-like assets.

More guidance may also be needed for money market funds and cash-focused ETFs.

“Any successful ISA reform must balance simplicity, fairness, and practical enforcement.” — UK Investment Industry Representative

ISA providers may also face additional work monitoring holdings and applying new rules correctly. As consultations continue, the final rules could still change, leaving uncertainty around how the loophole may work in practice.

What Are Financial Experts and Investment Platforms Saying About the Proposal?

Reaction from the investment industry has been mostly critical, with many experts arguing that holding cash inside a Stocks and Shares ISA is a standard part of portfolio management. Investors often keep cash temporarily while waiting for opportunities, receiving dividends, or planning withdrawals.

Main Concerns Raised by the Industry

- Administrative complexity: Providers may face extra reporting and monitoring requirements.

- Higher compliance costs: Platforms could see increased operational expenses.

- Investor confusion: More complicated rules may create uncertainty for retail investors.

- Lower ISA appeal: Some experts fear Stocks and Shares ISAs could become less attractive.

- Unclear rules: Questions remain around how cash-like assets may be treated.

“Complex tax structures risk discouraging participation rather than encouraging long-term investing.” — Public Policy Director, UK Investment Sector

These concerns suggest that implementation challenges may be as significant as the tax itself.

How Could the New ISA Rules Change the Way UK Savers Manage Their Money?

The proposed levy may alter how savers allocate their annual ISA allowance. Some individuals may increase exposure to equities and investment funds, while others could seek alternative tax-efficient strategies outside traditional ISA structures.

The treatment of money market funds will be particularly important, as these products are commonly used to preserve capital while generating modest returns.

The reforms could also increase demand for financial advice as savers seek clarity on how best to structure their portfolios under the new framework.

At the same time, the changes may reinforce the distinction between savings and investing. The Government’s position is that investment ISAs should primarily support long-term investment rather than functioning as high-capacity savings accounts.

Should You Make Any Changes to Your ISA Strategy Before the 2027 Deadline?

At this stage, caution is generally advisable. The proposed rules continue to attract debate, and several operational details remain unclear. Furthermore, reports indicate that some aspects of the wider ISA reform programme may face delays or revisions before implementation.

Rather than reacting immediately, investors may benefit from reviewing their current ISA structure, understanding how much cash they typically hold within investment accounts, and monitoring future announcements from HMRC and the Treasury.

For most savers, maintaining a diversified approach while staying informed is likely to be more sensible than making rushed decisions based on incomplete information. As regulatory details emerge, the picture surrounding the Rachel Reeves Investment ISA Levy should become much clearer.

Conclusion

The proposed Rachel Reeves Investment ISA Levy could significantly reshape how UK savers use Stocks and Shares ISAs from April 2027.

While the Government aims to encourage more investment and close perceived loopholes, the plans have sparked concerns over complexity, fairness, and unintended consequences.

With key details still under review, savers should stay informed, monitor HMRC updates, and avoid making major financial decisions until the final rules and implementation framework are confirmed.

FAQs About the Rachel Reeves Investment ISA Levy

Will existing ISA balances be taxed immediately when the new rules begin?

Current reports suggest the levy would apply from April 2027, but final HMRC guidance is still required to confirm how existing balances would be treated.

Does the proposed 22% levy apply to dividends and investment growth?

No. The proposal focuses on interest earned from uninvested cash rather than gains from shares, funds, or dividends.

Are money market funds likely to be treated differently from cash holdings?

This remains one of the biggest uncertainties. HMRC has not yet provided definitive guidance on all cash-like assets.

Can savers still use their full £20,000 ISA allowance after 2027?

Based on current proposals, yes. The overall ISA allowance remains £20,000 even though Cash ISA limits may change.

Will ISA providers need to change how they report cash balances?

Potentially. Many industry experts believe providers may need new systems to monitor and report qualifying and non-qualifying holdings.

Why was a similar tax charge removed from ISAs in 2014?

The earlier system was removed as part of reforms intended to simplify ISA rules and increase participation.

Could the Government delay or amend the ISA levy before implementation?

Yes. Ongoing consultation, industry feedback, and practical concerns could result in modifications before the planned 2027 start date.