Many UK pensioners are now paying tax on their retirement income due to frozen personal allowance thresholds and rising state pension payments.

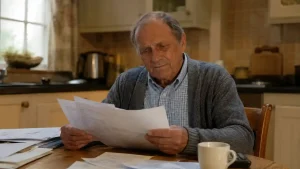

Alan Perkins’ case has drawn national attention after the 71-year-old retiree received an £800 tax bill despite relying mainly on his state pension and Serps contributions.

His story reflects growing concerns about fiscal drag, the triple lock and the financial pressure facing older Britons as more retirees are pushed into taxation without official tax rate increases.

Key Takeaways:

- Alan Perkins received an £800 tax bill despite having no private pension savings

- Frozen tax thresholds are pushing more pensioners into paying HMRC

- Serps payments increased Mr Perkins’ annual retirement income

- The state pension could exceed the personal allowance by 2027

- Fiscal drag is becoming a major concern for UK retirees

- Rising living costs are adding further pressure on pensioners

- Experts warn millions more pensioners could face similar tax issues in future

Why Is Alan Perkins Paying Tax on His State Pension?

Alan Perkins spent more than 50 years working multiple jobs to support his family before retiring. Much of his career was dedicated to working as a commercial heating engineer, often completing long overtime shifts and additional minicab driving work during evenings and weekends.

Like many workers of his generation, Mr Perkins joined the State Earnings-Related Pension Scheme (Serps), which allowed employees to build extra retirement income on top of the basic state pension. As a result, he now receives approximately £16,500 annually in retirement income.

The issue is that this amount exceeds the current personal allowance threshold of £12,570. Once income rises above this figure, tax becomes payable.

Although the tax threshold freeze was initially introduced by the Conservative Government in 2021, it has since been extended until 2031 under Chancellor Rachel Reeves. Critics argue this policy has become a stealth tax because incomes rise over time while tax allowances stay the same.

Mr Perkins expressed frustration about the situation, particularly after years of hard work and contribution to the system. He believed the state pension would provide financial security in retirement rather than lead to additional tax burdens.

A retirement adviser explained the growing concern among older Britons clearly: “I regularly speak to pensioners who are shocked when they receive a tax notice from HMRC. Many assumed their state pension would remain below taxable levels forever, but frozen allowances have changed that entirely.”

How Do Frozen Tax Thresholds Affect UK Pensioners?

Frozen tax thresholds are becoming one of the biggest financial pressures facing retirees across the UK. While tax rates themselves may not increase, keeping allowances unchanged during periods of rising incomes creates what economists call fiscal drag.

Fiscal drag occurs when people gradually move into higher tax brackets because wages or pension payments increase while tax thresholds stay fixed. This means taxpayers end up paying more without any official tax rise being announced.

For pensioners, the problem is particularly significant because the state pension increases every year under the triple lock policy.

The triple lock guarantees annual increases based on whichever is highest between:

- Inflation

- Average earnings growth

- 2.5 per cent

As pension payments continue to rise, more retirees are crossing the personal allowance threshold.

What Is Fiscal Drag and Why Does It Matter?

Fiscal drag allows governments to generate additional tax revenue quietly over time. Instead of raising tax rates directly, frozen thresholds naturally bring more people into taxation.

This policy has become politically controversial because many pensioners feel they are being penalised despite already facing higher living costs.

Financial planner David Lawson shared his concerns about the issue: “In my experience, retirees are often the least prepared for stealth taxes because they budget around fixed incomes. When thresholds remain frozen for years, even modest pension increases can suddenly create tax liabilities that people never expected.”

Why Pensioners Are Feeling the Pressure More Than Ever?

The cost-of-living crisis has already placed considerable pressure on older households. Rising food prices, higher energy bills and increasing housing expenses are making retirement more difficult for many Britons.

According to the Pensions and Lifetime Savings Association, the minimum annual income needed for a basic standard of living in retirement is around £13,400. Alan Perkins’ income sits only slightly above this level, despite being taxable.

For many retirees, this creates a difficult financial balance. Even though pension income may technically exceed the personal allowance, it does not necessarily provide a comfortable lifestyle.

What Was the SERPS Pension Scheme and How Did It Work?

The State Earnings-Related Pension Scheme, commonly known as Serps, was introduced in 1978 to help workers build additional retirement income alongside the basic state pension.

Employees who joined Serps paid extra National Insurance contributions during their working years. In return, they received additional pension payments after retirement based on their earnings history.

The scheme remained active until 2002 before being replaced by the State Second Pension. Eventually, both systems were phased out in favour of the new State Pension introduced in 2016.

For workers like Alan Perkins, Serps appeared to be a sensible decision at the time. The additional contributions promised improved financial stability in retirement, especially for those without substantial private pensions.

However, rising pension income now means some retirees are exceeding the personal allowance threshold and becoming liable for tax.

This situation has led many pensioners to question whether they are being unfairly punished for contributing more during their working lives.

Why Are More Pensioners Expected to Pay Tax by 2027?

Analysts believe millions more pensioners could begin paying tax over the next few years due to the interaction between frozen allowances and rising state pension payments.

The new State Pension is expected to increase to approximately £241.30 per week in April 2026. This would equal roughly £12,547 annually, only slightly below the current personal allowance of £12,570.

If annual increases continue under the triple lock while allowances remain frozen, the state pension could soon exceed the tax-free threshold entirely.

State Pension Rates Compared With the Personal Allowance

| Year | Estimated Full State Pension | Personal Allowance |

| 2024 | £11,502 | £12,570 |

| 2025 | £11,973 | £12,570 |

| 2026 | £12,547 | £12,570 |

Once pension income exceeds the allowance, retirees may need to pay income tax solely on their state pension payments for the first time.

This possibility has alarmed many campaigners and pension experts, who argue the system is becoming increasingly unfair to older citizens.

What Did Rachel Reeves Say About State Pension Tax?

During her Budget statement, Chancellor Rachel Reeves confirmed that frozen tax thresholds would continue until 2031. The decision immediately sparked criticism from financial experts and pension advocacy groups.

Ms Reeves previously stated that pensioners reliant solely on the state pension would not have to pay tax. However, critics argue that many retirees with modest additional pension income, such as Serps payments, are already facing tax bills.

The Treasury later clarified that pensioners whose only income comes from the basic or new State Pension without additional increments may receive administrative support to avoid small tax assessments from 2027 onwards.

Despite this clarification, concerns remain widespread.

Many pensioners believe the Government underestimated how many retirees would be affected by frozen thresholds. Others argue the policy unfairly targets older generations who spent decades contributing to the system.

Alan Perkins himself questioned whether policymakers fully understood the impact on ordinary retirees. His situation has become symbolic of broader anxieties surrounding retirement taxation in Britain.

How Is the Rising Cost of Living Impacting Retirees?

The financial pressure facing pensioners extends beyond taxation alone. Inflation and higher living costs continue to affect retirement budgets across the country.

Energy bills remain a major concern for older households, particularly for pensioners spending more time at home during colder months. Food prices and transport costs have also increased significantly over recent years.

For retirees living primarily on state pension income, even relatively small tax charges can create additional strain.

Many pensioners are now reassessing their retirement plans and reducing discretionary spending to manage rising costs. Some are also seeking financial advice to better understand their tax position and available support.

Charities supporting older people have warned that financial insecurity among retirees is becoming more common, especially for those without substantial private pensions or savings.

Could the Government Change Pension Tax Rules in the Future?

Pressure is growing on the Government to reconsider frozen tax thresholds and the future taxation of pension income.

Some analysts believe future governments may eventually raise the personal allowance to prevent millions of pensioners from entering taxation. Others argue broader pension reform may become necessary if the state pension continues rising under the triple lock.

Political debate around retirement taxation is likely to intensify as the number of affected pensioners grows.

Campaign groups are already calling for greater protection for retirees who rely mainly on state support. At the same time, Treasury officials face pressure to maintain tax revenues amid wider economic challenges.

Whether reforms are introduced may depend heavily on future economic conditions and public reaction.

What Can Pensioners Do to Manage Their Tax Position?

Although pensioners cannot avoid all taxation, there are practical steps that may help them manage their finances more effectively.

Retirees should regularly check their tax codes to ensure HMRC calculations are accurate. Incorrect tax codes can sometimes lead to overpayments.

Understanding all income sources is also important, including:

- State pension payments

- Workplace pensions

- Serps or additional pension income

- Savings interest

Some pensioners may benefit from professional financial advice, particularly if they have multiple income streams.

Careful financial planning can help retirees make better use of allowances and understand potential future tax liabilities before they become problematic.

Conclusion

Alan Perkins’ experience has become a powerful example of the financial challenges facing many UK pensioners today.

Despite decades of hard work and contributions through Serps, he now faces taxation on an income that only slightly exceeds the minimum level considered necessary for basic retirement living.

His case highlights how frozen tax thresholds, rising pension payments and increasing living costs are combining to place growing pressure on retirees across Britain.

With the state pension expected to rise further over the coming years, many more pensioners could soon find themselves paying tax for the first time. The debate surrounding retirement taxation is therefore unlikely to disappear anytime soon.

FAQs

Do pensioners pay tax on the state pension in the UK?

Yes, the state pension is considered taxable income. However, tax is only payable if total annual income exceeds the personal allowance threshold.

What is the personal allowance for pensioners in 2026?

The current personal allowance remains £12,570 and is frozen until 2031 unless future governments introduce changes.

What is fiscal drag in simple terms?

Fiscal drag happens when tax thresholds stay frozen while incomes rise, causing more people to pay higher levels of tax over time.

How does the triple lock affect pension tax?

The triple lock increases state pension payments annually, which can push retirees closer to or above the tax-free allowance.

What was the Serps pension scheme?

Serps was a government retirement scheme that allowed workers to build additional pension income based on earnings and National Insurance contributions.

Will the state pension become taxable for everyone?

Not necessarily, but experts believe more pensioners could become liable for tax if state pension increases continue while allowances remain frozen.

Can pensioners reduce their tax liability legally?

Some pensioners may reduce tax through proper financial planning, checking tax codes and using available allowances efficiently.